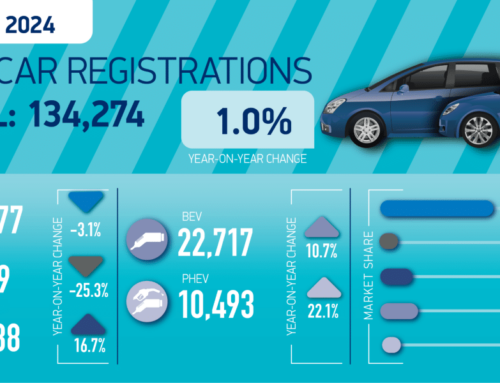

DESPITE healthy orders ahead of the March plate change, Cox Automotive is warning that further headwinds face the new vehicle manufacturing market, disappointing those looking forward to any projected recovery.

Global political events mean that the sector could well be heading towards continuing rapid changing market dynamics, similar to 2021.

According to Philip Nothard, Insight and Strategy Director at Cox Automotive, March’s new car registration results usually creates one of the highest volume months of the year. Despite the rapidly changing global political situation, Nothard said there are reasons to be optimistic, with healthy order banks for March registrations, albeit for specific manufacturers and particular models.

This could create an imbalance of profile of part-exchanges and future used vehicles entering the parc. The hope for Cox Automotive is that March will generate some much-needed used vehicles for the wholesale and remarketing sector and dealers.

Nothard referred to changes in retail where reports imply manufacturers are operating a ‘sold order only’ process or deciding to prioritise the retail channel, in addition to either limiting supply or offering no response to when production will resume. The topic of the Agency Model is also accelerating, and whilst some manufacturers may already have plans in place, others know they must do it but are not sure how.

Manheim February auction results

February’s wholesale key indicators continued to display signs of a stable market created by the ongoing imbalance between supply and demand, which has existed since the summer of 2020.

Manheim lanes last month experienced three key indicator increases. This was seen in the average first-time conversion, which increased by 0.74% to 84.40% month-on-month. In addition, the average age of cars sold also slightly increased by 1.2% to 102.1 months, and the average mileage of cars sold increased by -0.56% and up by 396 miles to 70,558 miles.

However, despite three key indicators experiencing month-on-month increases, used car values fell slightly, with the average sale price decreasing by 2.32% or £187, to £7,866. CAP Clean values also experienced a marginal month-on-month fall of 0.22%, to 98.04%.

Writing in Cox Automotive’s new Q1 2022 edition of AutoFocus magazine, Nothard said: “It’s increasingly likely that we will see a continuation of many of the market dynamics we saw in 2021. However, although there are signs of new vehicle supply returning, it is currently very dependent on those manufacturers who have managed to secure the necessary materials to build vehicles and therefore keep production lines running. And even then, those manufacturers can only fulfil quotas on select models and derivatives.

“While manufacturers are slowly getting to grips with their production issues, and the situation will improve as the year progresses, this will be a prolonged and gradual process. As a result, we will not see a flood of stock enter the market, but rather a gradual increase as the backlog of orders for new vehicles gets cleared, in turn generating much needed stock for the used market.”

Leave A Comment